This is the starting point for any calculation and one of the most important steps to achieving a realistic savings simulation. gross annual salary determines your initial taxable income, whereas your personal income tax bracket This defines the percentage of tax you will pay. Both factors directly influence how much you can save with flexible remuneration.

To begin, locate your gross salary on your contract or annual payslip. For example, if your salary is €30,000 gross per year, this is the value you'll use as a reference. From here, you must Identify which income tax bracket you are in, as each band applies a different tax rate. Knowing your band will help you more accurately estimate how much tax you will save when you reduce the taxable base thanks to flexible remuneration.

| Personal income tax brackets | Type of retention |

|---|---|

| Up to €12,450 | 19% |

| £12,450 – £20,200 | 24% |

| £20,200 – £35,200 | 30% |

| £35,200 – £60,000 | 37% |

| £60,000 – £300,000 | 45% |

| Over €300,000 | 47% |

Example applied to a gross salary of 30,000:

The relevant sections would be the following:

In this case, the salary of €30,000 falls within the bracket from €20,200 to €35,200, with a marginal rate of 30%. This does not mean that you pay a 30% for your entire salary., but only for the part of the salary that falls within that bracket.

This is how your taxation would be distributed:

The percentage corresponding to the last stage you are in is known as Marginal personal income tax, and it is key to calculating your potential savings with flexible remuneration.

Before continuing with the calculation, it is important to identify which flexible remuneration plan products benefit from tax exemption and up to what amount.

These limits determine the real savings you will be able to obtain and prevent you from exceeding the amounts permitted by regulations.

products you can choose from will depend on the Flexible remuneration plan implemented in your company.

Once you know your gross salary and your personal income tax bracket, the next step is to Decide how much you want to allocate to flexible benefits And how will this affect your taxable base? This decision will depend on the products offered by your company (such as food, transport, childcare or training) and the tax limits established for each.

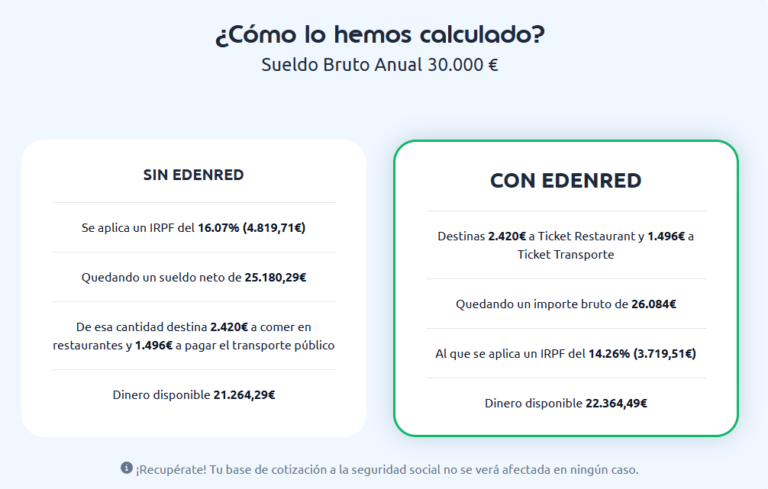

For example, if you decide to allocate 1,496€ for transport (the maximum that can be allocated per year) and €2,420 for food (€11/day for 20 days a month, for 11 months), A gross amount of €26,084 remains., What will be the new tax base.

To this tax base a personal income tax rate of 14.26% is applied, meaning you will pay €3,719.51 in income tax and have €22,364.49 in net salary remaining, with a saving of €1,100.20.

In a nutshell: