The flexible compensation has become one of the most effective ways for employees to increase their take-home pay without additional cost to the company. However, one of the most frequently asked questions is: how much can i save with flexible compensation? And above all how exactly do you calculate the savings?

In this article we explain it step by step, with practical examples and answering key questions. You will also find out how to use Edenred's flexible compensation calculator to obtain a accurate simulation in less than a minute.

Calculating flexible compensation savings step by step

1. Identify your gross annual salary and your personal income tax bracket.

This is the starting point for any calculation and one of the most important steps to get a realistic simulation of your savings. The gross annual salary determines your initial taxable income, whereas your personal income tax bracket defines the percentage of tax you will pay. Both of these factors directly influence how much you can save with flexible compensation.

To start with, locate your gross salary in your contract or annualised salary statement. For example, if your salary is 30.000 € gross per year, This is the value you will use as a reference. From here, you should identify which personal income tax bracket you are in, The tax rate for each tax bracket is different. Knowing your bracket will help you to estimate more accurately how much tax you will avoid paying when you reduce your tax base through flexible compensation.

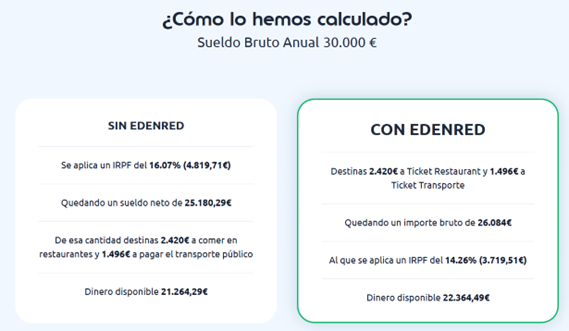

Example applied to a gross salary of 30,000:

The relevant sections would be as follows:

Up to 12,450 € → 19%

From 12.450 € to 20.200 € → 24%

From 20.200 € to 35.200 € → 30%

In this case, the salary of €30,000 falls into the bracket from €20,200 to €35,200, the marginal rate of which is €30,000. 30%. This does not mean that you pay a 30% for your entire salary., The taxable income of the employer is not the same as that of the employee, but only for the part of the salary that is in that bracket.

This is how your taxation would be distributed:

Up to 12,450 € → 19%

From 12,450 € to 20,200 € (7,750 €) → 24%

From 20,200 € to 30,000 € (9,800 €) → 30%

The percentage corresponding to the last tranche you are in is known as the Marginal personal income tax, and is key to calculating your potential savings with flexible compensation.

2. Check which products are exempt from personal income tax and their limits.

Before proceeding with the calculation, it is important to identify which products of the flexible compensation plan enjoy tax exemption and up to what amount.

These limits determine the actual savings you will be able to make and prevent you from exceeding the amounts allowed by the regulations:

3. Determine how much you will allocate to flexible compensation and calculate your new taxable income.

Once you know your gross salary and your personal income tax bracket, the next step is to decide how much you want to spend on flexible compensation and how this will affect your taxable income. This decision will depend on the products offered by your company (such as food, transport, childcare or training) and the tax limits set for each.

For example, if you decide to allocate 1,496 to transport (the maximum that can be spent per year) and 2.420 € to food (11€/day for 20 days per month, for 11 months), 26,084 gross remains, which will be the new tax base.

4. Calculate how much income tax you will pay and the final savings from flexible compensation.

In which flexible compensation products can I save the most?

Savings depend on the type of product and its level of tax exemption:

Restoration → significant savings due to the daily exemption

Public transport → depends on how much you use it, the more you use it, the more you save (up to 1,500 € per year exempted).

Nursery → as it is compatible with other state and autonomous community aid it is very advantageous

Health insurance → Depending on the policy you take out, you can save a lot of money.

If you want to compare savings between products, the Edenred's flexible compensation savings calculator will show you which is most beneficial for you.

Does flexible compensation affect my contribution?

No. Although you pay less personal income tax, you continue to pay contributions as usual, since the contribution is based on the total gross salary, not in the tax base after the application of flexible compensation.

This means that does not affect your pension, benefits or employment rights..

What happens if I do not spend the full allocation?

It will depend on the policy of each company, but in general:

On products such as catering or transport, if you do not consume the allocated amount, it may be lost or accumulated.

In childcare, spending is usually adjusted on a monthly basis, so there is usually no surplus or waste.